Blog

When Private Equity Meets the Data Center Gold Rush

Analysis

"What is past is prologue"

William Shakespeare, The Tempest

Shakespeare reminds us that today’s developments are echoes of choices made long ago. Nowhere is this more evident than in the unresolved status of Fannie Mae and Freddie Mac, whose 2008 rescue continues to shape mortgage rates, housing affordability, and political risk today.

Freddie and Fannie (F&F) have existed in a liminal state for more than 15 years. That unresolved status is the product of crisis-era decisions that stabilized markets in the short term, but quietly locked the housing finance system into a political and financial stalemate.

Now, as we begin a new year, with murmurs of a possible IPO circulating, investors and policymakers alike are once again asking:

What is the future of these institutions?

Fannie Mae was created in 1938 as part of the New Deal reforms, a response to the housing collapse that followed the Great Depression. Fannie’s role was to provide liquidity to a struggling mortgage market by buying up loans from lenders, which in turn freed up capital to fund more homebuyers. Freddie Mac was established later, in 1970, with a similar but more competitive mandate: to provide an alternative channel for securitizing mortgages and to help foster greater access to housing finance through a broader network of originators, including smaller lenders and thrift institutions.

For decades, they operated profitably and were seen as stabilizing forces in the housing market. From the outset, their success rested on a structural ambiguity; markets treated their obligations as government-backed, even though that guarantee was never made explicit.

But their continued profits built atop growing structural tension. The implicit backing guarantee from the U.S. government allowed them to borrow cheaply and grow rapidly, yet their risk management and regulatory oversight failed to keep pace. As the 2000s progressed, F&F began to take on greater credit exposure, especially during the subprime lending boom. As private-label securitization expanded in the early 2000s, F&F faced pressure, both political and competitive, to maintain market share and expand access to credit. That pressure pushed them toward greater exposure to riskier loan vintages late in the cycle, relative to their historical standards.

By the time the housing bubble began to deflate, the Government Sponsored Enterprises (GSEs) had amassed enormous exposure to deteriorating mortgage assets. Their holdings of subprime and Alt-A mortgages, many bundled into private-label securities or held directly in portfolios, magnified their vulnerability. When defaults began to spike, the fragility of their capital structures and overreliance on housing price growth became impossible to ignore.

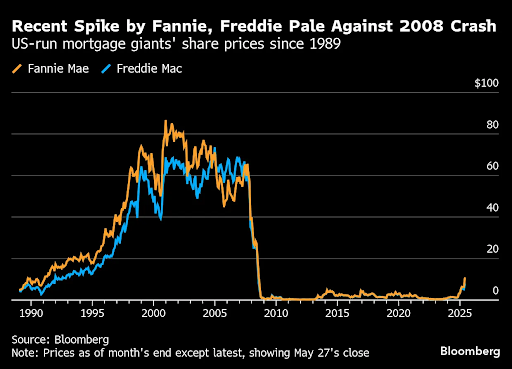

The financial crisis reached a critical stage in 2008. As mortgage defaults surged and the value of mortgage-backed securities plummeted, confidence in the solvency of Fannie Mae and Freddie Mac evaporated. Together, the two firms had more than $5 trillion in mortgage-backed securities and guarantees outstanding: nearly half of the entire U.S. mortgage market. The risks embedded in their portfolios were suddenly seen as systemic.

In July 2008, amid mounting losses and investor concern, Congress passed the Housing and Economic Recovery Act (HERA).

Conservatorship is a legal framework in which control of a distressed entity is transferred to a third party to restore stability. A familiar parallel can be drawn from the conservatorship of Britney Spears, where decision-making authority was centralized under the premise of protection. Over time, however, the arrangement raised difficult questions about duration, accountability, and the absence of a clear exit.

Conservatorship was not the only theoretical option; nationalization, liquidation, or an explicit guarantee were all possible. The main difference relative to all the other solutions was the ability to preserve market functioning while postponing the most sensitive political decisions.

That support became essential just weeks later. In September 2008, following another wave of steep losses and a sharp decline in their stock prices, the government placed both institutions into conservatorship.

Under this arrangement, the FHFA assumed control of management, and the Treasury injected capital through senior preferred stock purchase agreement (PSPAs). Under the PSPAs signed in September 2008,

Together, these terms ensured solvency but subordinated all private capital to the federal government. These conditions fundamentally reordered the GSEs’ capital structures. Treasury’s claims were senior to all other equity, while dividends to common and junior preferred shareholders were suspended indefinitely. Although the Treasury did not immediately exercise its warrants, the structure effectively gave the federal government economic control without formal nationalization.

Although conservatorship was framed as a temporary “time-out,” the PSPAs transferred nearly all financial upside and effective control to the federal government. What was presented as a temporary stabilization framework would soon harden into a durable and politically convenient operating model.

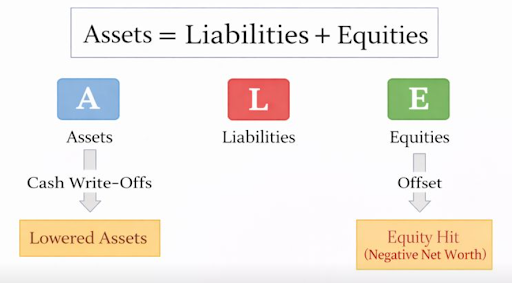

By 2009, Fannie Mae and Freddie Mac were trapped in a self-reinforcing financial loop created by the mechanics of conservatorship itself. In the years immediately following conservatorship, Fannie Mae and Freddie Mac continued to rely heavily on Treasury support. Importantly, this dependence was not driven primarily by ongoing operating losses. Instead, it reflected a series of accounting decisions that eliminated the enterprises’ reported capital.

Under the direction of the FHFA, the GSEs took aggressive non-cash charges, including large write-downs of deferred tax assets and the build-up of substantial loan loss reserves in anticipation of future defaults. Critically, these losses were largely non-cash. While these actions were defensible from a conservative accounting perspective, they had a decisive consequence: they rendered both enterprises insolvent on a GAAP basis, even as underlying cash flows began to stabilize.

These accounting losses forced F&F to draw capital from the Treasury in order to meet regulatory requirements. By 2012, the two firms had drawn a combined $187 billion under the Preferred Stock Purchase Agreements. Each draw, however, came with significant conditions. Every dollar borrowed increased the liquidation preference of Treasury’s senior preferred shares and triggered a fixed 10 percent annual dividend obligation.

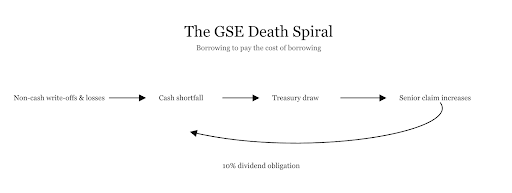

This structure created what became known as the “GSE death spiral,” a self-reinforcing financial loop. Accounting write-downs wiped out reported capital, forcing Treasury draws.

Those draws increased future payment obligations to the government. Because F&F lacked sufficient earnings at the time, they were required to borrow additional funds simply to service those obligations.

Each Treasury draw increased the size of Treasury’s senior claim, raising future dividend obligations and making capital restoration impossible under the existing structure: The dynamic was akin to a borrower using new debt to service old debt: just digging yourself in a further hole. Absent a structural change, the conservatorship framework risked consuming its own backstop.

To prevent this outcome, Treasury and the FHFA amended the PSPAs multiple times between 2009 and 2012, expanding the size of Treasury’s commitment. The most consequential change came in August 2012 with the Third Amendment, which replaced the fixed 10 percent dividend with a variable dividend equal to nearly all of each enterprise’s net worth. This eliminated the dividend-driven draw cycle, but only by preventing the GSEs from retaining capital altogether.

This policy, known as the Net Worth Sweep, fundamentally altered the trajectory of conservatorship.

The Third Amendment to the PSPAs, implemented in August 2012, replaced the fixed 10 percent dividend owed to Treasury with a variable dividend equal to nearly all of F&F’s net worth above a minimal capital buffer. This policy was presented as a technical solution to the escalating draw-dividend cycle that had emerged under conservatorship. By eliminating fixed dividend obligations, Treasury and FHFA argued, the GSEs would no longer need to borrow simply to service government payments.

In practice, the Sweep fundamentally altered the economics of conservatorship. After 2012, Fannie Mae and Freddie Mac were no longer operating under a temporary stabilization framework, but under a structure that permanently transferred all upside to the federal government. Rather than allowing Fannie Mae and Freddie Mac to retain earnings and rebuild capital, it required that virtually all profits be remitted to the Treasury indefinitely.

The timing of this change would prove consequential.

Beginning in 2013, the GSEs entered a period of extraordinary profitability. As housing markets stabilized and credit performance improved, F&F reversed tens of billions of dollars in prior loss provisions and deferred tax asset write-downs that had been booked during the depths of the crisis. These reversals, combined with improving mortgage fundamentals, produced record earnings.

In 2013 alone, Fannie Mae and Freddie Mac generated more than $132 billion in combined net income. To place that figure in context, it rivaled or exceeded the annual profits of some of the most successful corporations in history, not because the GSEs had taken on new risk, but because previously impaired assets recovered as expected. These profits did not reflect a renewed appetite for risk, but the reversal of losses booked under crisis-era assumptions.

Yet under the Net Worth Sweep, none of these profits were retained. Every dollar was transferred to the Treasury. By 2018, cumulative payments to the government exceeded $240 billion, far surpassing the roughly $191 billion that had been drawn during the crisis. Despite this, the liquidation preference associated with Treasury’s senior preferred shares remained intact, and the GSEs were left with virtually no capital.

Subsequent disclosures reinforced the significance of the peculiar timing. Internal communications and deposition testimony revealed that officials within Treasury and FHFA were aware that a return to profitability was imminent when the Sweep was implemented. In one unsealed deposition, Mario Ugoletti, a senior FHFA official, referred to this period as a “golden era” for Fannie Mae and Freddie Mac, underscoring that their financial recovery was not unexpected.

The Net Worth Sweep resolved the immediate mechanical problem of the draw-dividend cycle, but only by foreclosing any path to capital accumulation. What had begun as a technical fix now carried permanent economic consequences, setting the stage for years of legal and political challenge.

As Fannie Mae and Freddie Mac continued to generate billions in annual profits under the Net Worth Sweep, shareholders began to challenge both the legality and the fairness of the arrangement. Common and preferred shareholders argued that the Treasury and FHFA had exceeded their statutory authority, violated contractual commitments, and, in some cases, infringed constitutional protections. Across jurisdictions, courts were willing to scrutinize process and governance, but consistently declined to unwind crisis-era policy choices.

Beginning in 2013, more than a dozen lawsuits were filed across federal courts. Plaintiffs sought a range of remedies, including the invalidation of the Net Worth Sweep, restoration of capital retention, and limits on the government’s control over F&F. Collectively, the cases tested how far emergency powers extended once the immediate crisis had passed.

Judges repeatedly signaled concern that unwinding the Sweep would amount to judicially rewriting financial crisis policy.

By the early 2020s, litigation had clarified the boundaries of conservatorship without offering an exit. The courts effectively signaled that any comprehensive resolution, whether a release from conservatorship, a restructuring of Treasury’s stake, or a reversal of the Net Worth Sweep, would need to come from the legislative or executive branches, not the judiciary.

Momentum around the future of Fannie Mae and Freddie Mac shifted decisively following the 2024 U.S. presidential election. Donald Trump’s return to the White House revived long-standing debates over housing finance reform, particularly unfinished efforts from his first term to release the GSEs from conservatorship. While no immediate policy change was announced, the election altered expectations about the direction of federal housing policy.

That shift became more pronounced with the appointment of Bill Pulte as Director of the FHFA. Pulte’s early public statements were widely interpreted by markets as signaling a more aggressive lean toward restructuring the GSEs’ ownership and capital framework. Rather than emphasizing indefinite conservatorship, FHFA leadership suggested renewed openness to recapitalization and a potential return to public markets.

Investor response was swift. After years of stagnation, the thinly traded common shares of Fannie Mae and Freddie Mac surged more than 700 percent from their pre-election levels. By late 2025, their combined market capitalization had increased from roughly $2.5 billion to more than $20 billion. While still modest relative to the size of the mortgage market they support, the move reflected a re-pricing of political risk rather than a reassessment of near-term earnings. Markets were not responding to a defined policy roadmap, but to the possibility that a long-frozen policy regime might suddenly change.

Behind the scenes, reports indicated increased coordination between the FHFA and the U.S. Treasury, now led by Secretary Scott Bessent, on potential paths toward partial privatization. In this context, an ‘IPO’ would not resemble a conventional full privatization, but rather a partial equity issuance designed to introduce private capital while preserving federal control.

According to reporting by major financial outlets, policymakers explored scenarios involving a limited public offering, potentially selling 5 to 15 percent of equity to raise new capital while retaining federal control in the near term. Valuation estimates for such an offering varied widely, with some discussions placing the combined enterprise value in the hundreds of billions. These estimates reflected not disagreement over earnings, but uncertainty over capital structure, guarantee pricing, and long-term ownership.

These developments were not without controversy. In mid-2025, Democratic lawmakers raised concerns that a rushed privatization could undermine the GSEs’ housing affordability mission or recreate pre-crisis incentives, where private shareholders captured upside while taxpayers bore systemic risk. The debate resurfaced a longstanding policy dilemma: whether the implicit government guarantee should remain in place, be made explicit and priced, or be reduced over time.

Should private shareholders capture upside in an institution whose liabilities markets still treat as government-backed?

By late 2025, policymakers signaled interest in a more gradual approach to reform. Rather than a full and immediate release from conservatorship, discussions centered on the possibility of introducing private capital through a minority equity sale, while retaining federal control as a stabilizing backstop. This proposed strategy echoed the post-crisis unwind of institutions such as AIG, where government ownership was reduced incrementally rather than through a single, decisive transaction.

The defining feature of the present was not a concrete plan, but the breakdown of the political stalemate that had defined the prior decade.

With the federal government’s warrants set to expire in 2028, the coming years represent a critical inflection point. The expiration serves as another checkpoint in a long series of unresolved decisions, one that could increase pressure on policymakers to act, but does not by itself determine whether the GSEs exit conservatorship or remain under hybrid public control. The question is no longer whether change is possible, but what form it takes and at what cost.

At the core of the debate is capital. Any meaningful release from conservatorship requires F&F to hold sufficient equity to absorb housing market shocks without immediate federal support. Rebuilding that capital base is not trivial. Decades of retained earnings were effectively swept away under the Net Worth Sweep, leaving F&F thinly capitalized relative to the scale of risk they guarantee. Any path out of conservatorship requires policymakers to choose how risk is priced, who bears it, and how much stability the housing system is willing to trade for market discipline This leaves us with 3 realistic paths.

Changes to the GSEs’ capital structure and risk profile will influence mortgage rates, underwriting standards, investor appetite for agency securities, and ultimately housing affordability. Each path carries real consequences beyond the balance sheet. Given that Fannie Mae and Freddie Mac support more than 70 percent of new U.S. mortgage originations, even modest policy shifts can ripple across the $12 trillion housing market.

The future of the GSEs is therefore not merely a question of privatization versus public control. It is a test of whether the U.S. housing finance system can reconcile financial discipline with its social mandate. The longer reform is deferred, the more the housing finance system relies on ambiguity rather than effective and efficient design.

The past, as Shakespeare warned, is indeed prologue.

What remains uncertain is whether policymakers will write a new chapter or continue revising the same old one.

Blog

Analysis

Blog