Analysis

Why Can’t America Build Affordable Housing?

Analysis

Downtown Washington is undergoing a quiet but consequential reset. Office vacancy remains historically elevated, with aging office buildings disproportionately affected by federal footprint consolidation and hybrid work patterns. At the same time, the city faces persistent housing affordability pressures, particularly near transit-rich corridors.

Downtown has empty floors and scarce housing. The disconnect is obvious. If Washington has excess office space and a persistent need for housing, why not convert one into the other?

On paper, it looks straightforward. In practice, it rarely pencils.

Growing up in the Washington area, downtown followed a predictable rhythm. Federal agencies and law firms filled office towers by mid-morning. At lunch, lines spilled onto sidewalks along K Street and Pennsylvania Avenue. By early evening, corridors emptied as commuters dispersed into Maryland and Northern Virginia. For decades, downtown’s rhythm was defined by work.

That rhythm evolved as residential towers rose alongside office buildings. Restaurants extended beyond the traditional 9 to 5 crowd. Downtown felt more mixed and resilient.

In the post-pandemic years, the city has grown quieter. Office lobbies that once operated at full capacity now sit half empty as many employees continue working from home. “Lease Now” banners stretch across many old office facades. Foot traffic has thinned, particularly in corridors dominated by mid-century office stock.

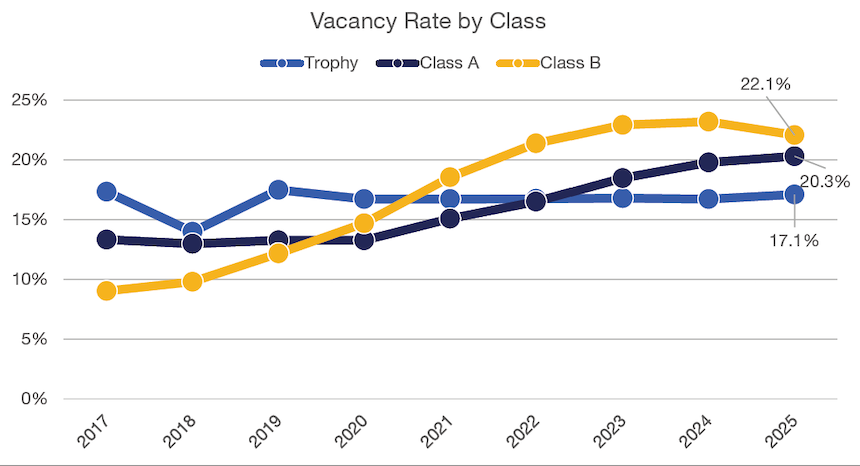

Broker data from Colliers confirms what is visible at street level. Washington’s overall office vacancy rate has remained above 20 percent in recent quarters, more than double its pre-2020 average. The burden is uneven. Class A trophy buildings continue to attract tenants, reflecting a sustained flight to quality, while older Class B and C inventory bear disproportionate vacancy. Cumulative net absorption since 2020 remains negative.

Federal agencies have also reduced square footage per employee and adopted hybrid workplace models, removing consistent daytime density from downtown corridors. Private tenants have downsized in parallel.

The consequences extend beyond leasing metrics. Reduced occupancy weakens street-level retail and reshapes neighborhood perception. Property values adjust accordingly. Washington is not alone in this adjustment. Cities such as San Francisco, Chicago, and New York are confronting similar imbalances between aging office supply and urban housing demand. However, as a federal city with a highly concentrated office core, the effects are particularly visible.

At a glance, conversion looks like a two-for-one fix. If downtown contains millions of square feet of underutilized office space while the city faces housing shortages, conversion appears efficient. The buildings exist, the infrastructure is already in place, and transit access is strong.

Office space, however, does not cleanly translate into housing.

Most vacant offices were designed for tenant density, with centralized cores and deep, uninterrupted floorplates. Residential buildings operate under different constraints. Units require daylight, distributed plumbing, acoustic separation, and individualized layouts. What appears as surplus square footage often conceals structural configurations that are costly to rework into unitized layouts.

The financial side is equally restrictive. Many aging Class B office buildings still carry debt structured around pre-2020 valuations and lower interest rates. Refinancing into a higher-rate environment compresses equity and limits flexibility.

Even when acquisition pricing falls to reflect distress, conversion requires substantial new capital at a time of elevated construction costs and tighter lending conditions. Hard costs, mechanical reconfiguration, and extended timelines introduce execution risk. In highly leveraged projects, modest cost overruns or delays can erase projected returns.

Vacancy alone does not determine feasibility.

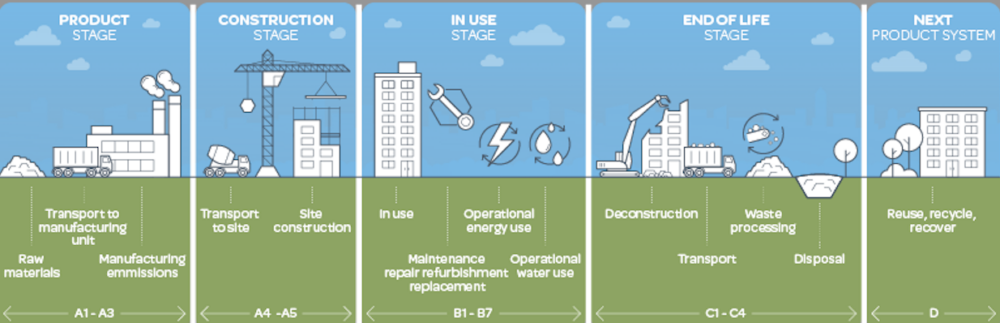

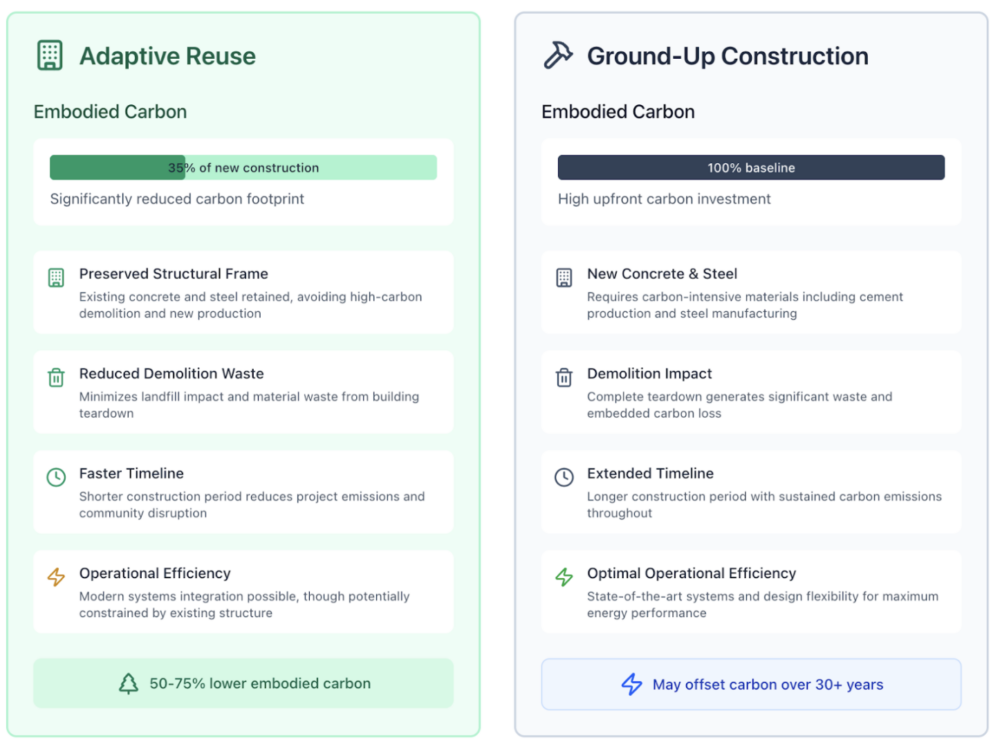

All buildings carry embodied carbon, the emissions generated through the extraction, manufacturing, transportation, and assembly of construction materials. Much of that carbon sits in the steel and concrete of the structural frame. Demolition adds emissions and resets the materials clock. Adaptive reuse keeps that carbon in place.

As architect Carl Elefante put it, “the greenest building is the one that already exists.”

Lifecycle studies suggest that reusing an existing structure can reduce embodied carbon emissions by roughly 50 to 75 percent compared to demolition and new construction, especially when the primary structural frame is retained.

Yet embodied carbon is only part of the equation. Operational emissions over decades of use can outweigh initial savings if retrofits fail to improve efficiency. Deep renovations that require significant structural intervention may narrow the environmental advantage.

The buildings that preserve the most embodied carbon are often the hardest to reposition financially.

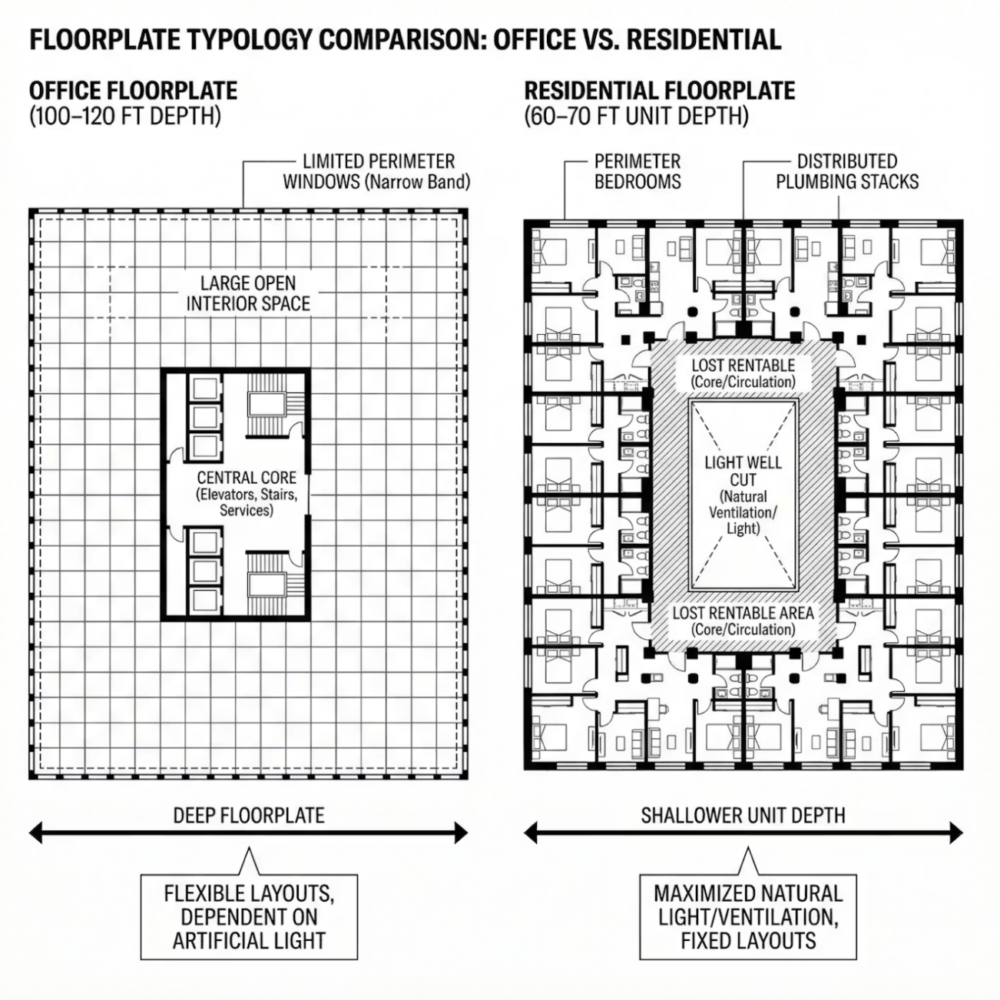

The same concrete frame that preserves embodied carbon can also limit residential design. The constraints begin with how office buildings were originally designed.

Most postwar office buildings were designed to maximize workforce density. Deep floorplates, often 90 to 120 feet from window to core, allow for large, uninterrupted workspaces. Centralized elevator banks and service cores reinforce that efficiency.

What worked in open-plan offices often results in deep, low-light unit layouts. Residential buildings operate differently. Bedrooms require direct access to daylight. Units must be shallower to avoid dark interior corridors. Kitchens and bathrooms must align vertically for plumbing efficiency.

To introduce daylight, developers often carve interior courtyards or light wells into the structure. These interventions make housing possible, but they reduce rentable area. In some cases, 10 to 20 percent of the floorplate is lost to achieve viable layouts. That lost area reduces revenue while costs remain largely fixed.

Ceiling heights and windows pose another challenge. Once new mechanical systems are installed, the available height may fall below contemporary residential expectations. Window spacing designed for office modules can result in awkward unit configurations.

Even when the geometry is workable, construction introduces volatility. Converting an office building into housing requires distributed plumbing risers, electrical reconfiguration, fire separation upgrades, and often complete mechanical replacement.

The real test begins once demolition starts. Interior walls and ceilings conceal decades of alterations. Hazardous materials, structural reinforcements, or obsolete systems may emerge only after work is underway. Delays increase carrying costs and financing exposure.

Ground-up multifamily development, while more carbon intensive upfront, offers developers a clearer construction process. Floorplates are optimized, systems are designed for residential use from the outset, and unknown structural conditions are rare. Adaptive reuse rarely offers the same predictability.

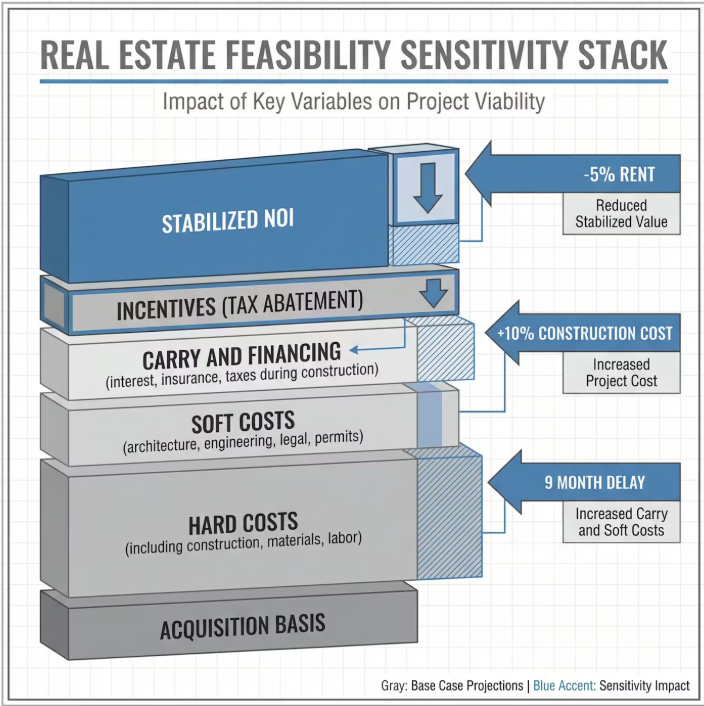

Underwriting is highly sensitive to small deviations. A 10 percent increase in hard costs or a nine-month delay can materially compress projected returns. That sensitivity is why many deals die in the middle, not at acquisition or exit.

Many aging office buildings were financed at pre-2020 valuations in a lower interest rate environment. Refinancing in today’s higher-rate environment compresses equity and complicates acquisition pricing. Even when buildings trade at a discount, conversion requires substantial new capital.

Part of the appeal of conversion lies in cap rate differentials. Stabilized multifamily assets in Washington typically trade at lower capitalization rates (or higher multiples) than aging Class B office properties. A building valued at an 8% cap rate as an office may command closer to 5.5% once repositioned as housing. The same stabilized income stream trades at a higher multiple.

That spread creates potential. A building producing $4 million in net operating income (NOI) is worth $50 million at an 8% cap rate, but roughly $73 million at 5.5%. In theory, repositioning unlocks value.

The challenge is that conversion costs can consume the spread. The arbitrage holds only if acquisition pricing falls far enough and construction costs remain controlled. If total development costs approach stabilized multifamily value, the margin disappears.

Recognizing the scale of downtown vacancy and the limits of private viability, Washington launched the Housing in Downtown initiative to incentivize office-to-residential conversions within a defined central business district geography. The program provides a 20-year property tax abatement for eligible projects that convert obsolete office buildings into residential use.

The initiative targets several million square feet of obsolete office space within the downtown core. The objective is to remove obsolete inventory and add residents with the goal of stabilizing retail, transit ridership, and the tax base. The abatement sacrifices near-term tax revenue in exchange for the possibility of long-term downtown stabilization

From an underwriting perspective, the abatement functions as gap financing. Property taxes represent a significant operating expense in multifamily assets. Reducing projected tax liability increases stabilized net operating income. Higher NOI expands loan capacity and can reduce required equity contributions. In feasibility models, this can shift certain projects from marginal to financeable.

However, the incentive does not alter physical constraints. It does not reduce floorplate depth, increase ceiling height, or eliminate the cost of structural modification. Nor does it eliminate construction and leasing volatility. If hard costs escalate or lease-up underperforms, the improvement in operating income may not offset execution risk.

The Housing in Downtown initiative narrows the feasibility gap but does not eliminate it. The program is most effective where configuration, acquisition basis, and construction discipline already provide a plausible path to stabilization.

Downtown Washington has been a story of re-adjustment. Office demand has recalibrated. Older inventory faces functional obsolescence. Housing demand persists. Climate objectives add pressure to reduce demolition and material waste.

Adaptive reuse sits at the intersection of these forces.

The environmental case is compelling. Preserving embodied carbon and limiting demolition align with decarbonization goals. The urban case is equally intuitive; adding housing to the core can stabilize retail, transit, and the long-term tax base. The market case, however, remains tentative.

Conversions work when acquisition pricing reflects distress, floorplates accommodate a residential layout, and construction risk remains contained. Incentive programs such as Housing in Downtown can narrow feasibility gaps, but they cannot override constraints embedded in the concrete and steel of the building.

Washington’s experience turns the debate into a screening exercise: which buildings can convert without destroying the economics. Some structures can transition from workplace to housing with limited intervention. Others require such extensive modification that financial and environmental returns narrow at the same time.

The greenest building may already exist, but only a subset of buildings will align with capital markets, construction realities, and long-term performance standards.

Conversions work, but only when the building and the balance sheet cooperate.

Analysis

Analysis

Blog